The Federal Reserve increased interest rates in December, and has plans for several more such increases in 2017. What does this mean for real estate?

The Fed Acts — But is Still Cautious

A year ago the Federal Reserve foresaw four rate rises in 2016. None happened — until the one in December. That year-long delay between rate increases was partly a reaction to recent events – but it also seems to have resulted from a gradual acceptance by Fed officials that low rates have become a longer-lasting feature of the economy.

A year ago unemployment was already low at 5%. The economy has recently created an average of 188,000 jobs per month. Job creation is once again pushing unemployment down; it now stands at 4.6%, the lowest rate recorded since August 2007. That is below its long-run sustainable level, according to at least 13 of 16 Fed rate-setters who penned forecasts in September.

Fed hawks thus argue that little slack remains in the labor market. The incoming Trump administration has taken aim at job outsourcing, yet in fact fewer workers were laid off or fired in September than in any month since data started being collected in 2000.

Inflation risk is also starting to tilt upwards. Congress is expected to cut taxes next year. Higher rates may be needed to stop any fiscal stimulus from becoming inflationary. Since the election, the inflation expectations of the markets have continued on an upward trend that began in September.

How Might Real Estate Be Affected?

Claim up to $26,000 per W2 Employee

- Billions of dollars in funding available

- Funds are available to U.S. Businesses NOW

- This is not a loan. These tax credits do not need to be repaid

The era of ultralow mortgage rates is likely over. The Federal Reserve’s decision to raise the federal-funds target rate by a quarter of a percentage point Wednesday probably means that borrowing is about to get more expensive for real estate borrowers.

What does this mean for real estate investors? Aren’t lower rates better for real estate prices, and higher rates worse?

Cap Rates and Interest Rates Don’t Necessarily Move Together

The relationship doesn’t appear to be that simple. If the economy is doing well and incomes are going up, people can afford more and they’re willing to take a bigger mortgage. Real estate cap rates also depend on credit availability, the supply-demand dynamic, and inflation. “Intuitively, you’d think that if interest rates go up, [then] house prices go down. But they don’t,” said Mark Palim, vice president for applied economic and housing research for Fannie Mae. Values might still go up, even if interest rates increase – although some would argue that increased interest rates will lead to higher expenses, and thus lower net operating incomes (and thus lower rates of return). In commercial real estate, too, sources such as Morgan Stanley caution that there are a lot of other variables besides just a singular focus on the connection between interest rates and cap rates.

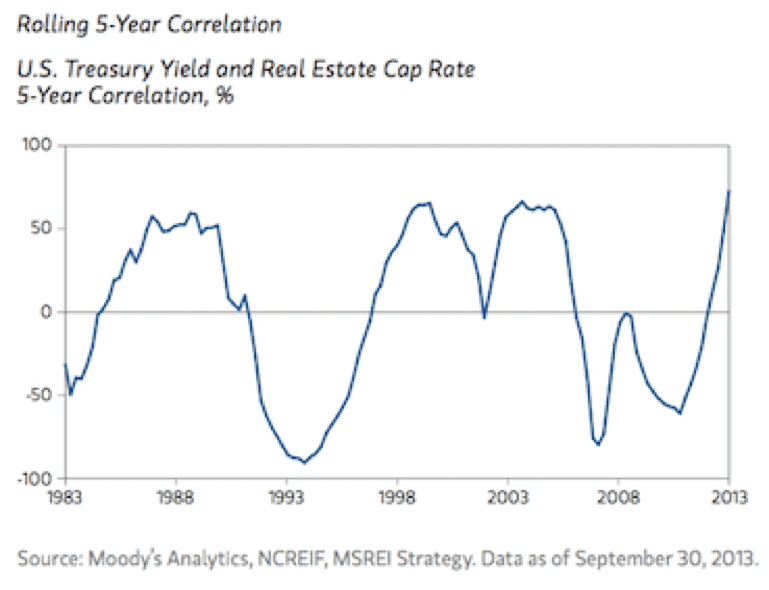

From a pure technical / quantitative point of view, there is in fact very little correlation historically between cap rates and changes in the 10-year U.S. Treasury rates. There have been various episodes where cap rates have not moved in the same direction as U.S. Treasury yields. Moreover, as shown in the above chart, the 5-year rolling correlation also varies considerably over time. There is also significant dispersion over various time horizons, as Morgan Stanley found in a recent report. Finally, an episodic analysis of eight key periods where the 10-year Treasury rate moved upward revealed that, in five of these instances, cap rates actually moved in the opposite direction.

In addition, there was until recently a historically relatively large difference, or “spread,” between cap rates and 10-year Treasury yields – more than 100 basis points above historical norms. That extra spread should be able to absorb a small an increase in 10-year Treasury yields and/or a further reduction in cap rates before property values should be affected. That historical spread margin can be viewed as somewhat of a protective “buffer” from the expected rise in interest rates. Strong global demand for U.S. Treasuries also seems to be keeping a lid on yields, despite tightening on the short end of the yield curve.

Improved Rents and Occupancy Rates Can Offset Increased Purchase Costs

More importantly, real estate returns do not depend solely on purchase prices, but are intimately tied to rents and property values. These generally improve in a strengthening economy. Rising mortgage rates may indeed increase the costs of purchasing properties – but on the flip side, an improving economy means property owners could benefit from higher occupancy rates and rents, which increase the value of real estate.

Despite anemic growth, the national unemployment rate has dropped to below 5%. Even with modest wage growth and tepid GDP growth, commercial property performance has benefited from job growth and constrained construction activity. Occupancies, rent and NOI growth have been solid and are expected to continue thriving in the quarters ahead.

Common underwriting practices should also mitigate investor worries. Property valuations usually assume a holding period increase of 50 to 100 basis points in the cap rate over the initial acquisition rate. This practice typically reflects the aging (finite life) of the property. As a result, cap rate increases are typically accounted for in return expectations, eliminating some of the potential surprise associated with them. So, investors should not fear cap rate increases that they expect — only the ones that they do not anticipate.

Finally, real estate performance is less sensitive to cap rate changes as the investment horizon lengthens. Time has the potential to heal many wounds from rising cap rates through the magic of compounding annual NOI growth rates. NOI growth can have a powerful impact on property values; the stronger the growth, the greater the protection against adverse movements in cap rates. This last point has important implications for property and market selection, and suggests that investors may do well to exhibit a preference for investments with solid NOI growth.

Author Bio

Lawrence Fassler is the corporate counsel of RealtyShares, a leading online real estate marketplace. Previously he served as the general counsel for another prominent real estate finance company; had run a real estate construction firm; and had worked for over 15 years as an attorney with prominent New York and Silicon Valley law firms (Shearman & Sterling and Cooley). Lawrence also earlier served as the general counsel for a Bay Area medical device company that was ultimately acquired for over $4 billion. Lawrence holds Series 7 and 66 licenses, and has a BS in Mechanical Engineering from UC Berkeley and a joint JD/MBA from Columbia University.

{kind=link}