Real estate prices, as with most financial markets, tend to follow a pattern. For the purpose of this article, we’ll call this pattern “The Real Estate Cycle.” There are many theories out there about The Real Estate Cycle, but the one I like best is called “The Great 18-Year Real Estate Cycle.” Back in the 30’s a real estate economist named Homer Hoyt discovered that real estate prices seemed to ebb and flow on an almost perfect 18 year schedule. Hoyt’s theory was later used and refined by now famed economist Fred E. Foldvary to predict the real estate crash of 2008. I’ll get into more depth about “The Great 18-Year Real Estate Cycle” shortly, but to me the important part isn’t necessarily the 18 year time frame, it is understanding that real estate market operates in a fairly predictable cycle that can be seen and taken advantage of by smart investors.

The Great 18-Year Real Estate Cycle

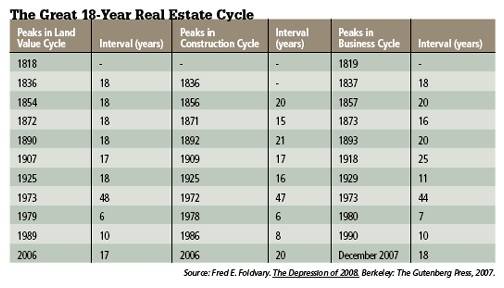

As I previously mentioned, The Great 18-Year Real Estate Cycle was originally discovered by economist Homer Hoyt. Hoyt noticed that the Chicago real estate market followed an almost perfect 18 year cycle dating back nearly 100 years. Here is a chart showing the cycle through 2007:

As you can see the 18 year cycle theory looks great until that huge gap between 1925 and 1973. Remember, though, that Hoyt discovered his theory in the 30’s, and at that point the 18 year cycle was nearly flawless. If you were expecting a perfect cycle that allowed you to precisely time your investment and make a ton of money with no risk – sorry to disappoint. Perfect business cycles just doesn’t exist – if they did the nature of capitalism would distort them. The important part isn’t necessarily the time frame, though, the important part is that you understand the leading indicators signaling when the cycle is turning.

Claim up to $26,000 per W2 Employee

- Billions of dollars in funding available

- Funds are available to U.S. Businesses NOW

- This is not a loan. These tax credits do not need to be repaid

The chart above, was used by Fred E. Foldvary – in his now famous report – to predict the recession of 2008. If you look again at the chart, you will notice that the 2008 prediction was right in line with the 18 year cycle – which Foldvary uses as the basis for his report. In his report, Foldvary even explains why Hoyt’s 18-year cycle theory diverged so drastically between 1925 and 1973. Foldvary points out that the cycle does not always function on a precise 18 year schedule, but – baring catastrophic events like a world war – for the most part the cycle should be right around 18 years. I’m not going to go in depth into all the various factors discussed by Foldvary in his report, but if you want to know more, I encourage you to read Foldvary’s full 40 page brief.

For those investors looking for a quick summary, here is an excerpt from an Editorial written by Foldvary which covers most of his key points he uses in the full report to validate his theory (note this was written in 2006):

“The real estate cycle world-wide follows a consistent pattern. There is first an expansion of money and credit by the monetary authorities. That expansion artificially reduces interest rates, which then increases borrowing for long-duration capital goods such as real estate construction, as well as the purchase of real estate. The expansion of the economy reduces vacancies and then raises rentals and real estate prices. Speculators then jump in to profit from this increase, adding to the demand and accelerating the increase in land values. The expansion of money causes price inflation, so the authorities cut back on the money expansion, raising interest rates.

Higher interest rates and higher prices for real estate then reduce business profits, reducing the rate of increase in investment in new capital goods. Note that at first, investment is still expanding, but it expands at a slower rate. The negative rate of increase eventually makes growth negative also, and output falls. Rising interest rates increases mortgage payments, and as prices and equity no longer increase, those who can barely afford a house or condominium and bought with minimum payment plans have to sell. Rising unemployment also increases foreclosures. Real estate speculators switch to buying foreclosures at below-market rates and flipping them for quick sale to naive buyers who don’t understand the real estate cycle.

At first, sales of residential real estate slow down, but owners stubbornly refuse to lower the price, so the inventory of unsold house rises. In California, where house prices have about doubled during the past 5 years, house sales have decreased 29 percent from October 2005 to 2006. Non-residential real estate construction is now also slowing down. While media attention is on residential real estate, commercial real estate is actually more important for the real estate cycle, as business investment in capital goods, including non-residential construction, drives the cycle as high real estate prices and higher interest rates make investment less profitable. We are now seeing a reduction in manufacturing, accompanied by factory shut downs. Non-residential construction fell in October 2006, while residential construction had already been falling.”

Now that the history lesson is over, let’s get to the part that investors really care about – where are we now, and how can you make money from this? If you look strictly at the 18 year pattern, the next peak will happen sometime in the mid 2020’s – so we still have a few years. Rather than focusing on the date, though, I encourage investors to look at the fundamentals. If you dive deeper into the fundamentals you will notice that the market has for the most part leveled out. In most real estate markets across the country home prices aren’t really increasing, but the huge drops seem to be a thing of the past. If you look at affordability indexes you’ll notice how buying a home actually makes sense now – which was not the case a few years back. In fact, in many real estate markets it is actually cheaper to buy a home now than it is to rent. Interest rates are at all time lows, and mortgages are as attractive as they have ever been.

Now I’m not predicting home prices to start climbing 20% like they did back in the height of the bubble, but investors shouldn’t be banking on that anyway. Smart investors in today’s market can see that with mortgage rates ridiculously low, and property prices back at reasonable levels, they can purchase homes at extremely high cap rates – which means cash flow. They aren’t banking on appreciation to make money – they are making money every month from rental income.

Let’s assume that the next peak will happen sometime around 2025 – that gives us about another 13 years before the bubble pops to take advantage of the down part of the real estate cycle. Want to know a good plan for retirement? How about you buy as much property as you can, ride out the next 10 years enjoying your cash flow, and then sell when the market starts to peak again in the mid 2020’s? Sure beats working till you’re 80, which by the way, is what some experts believe the new retirement age needs to be – scary huh?

{kind=link}